Another “bipartisan” bill is promising to screw the little guy—yet again.

On July 21, 2025, the Equal Opportunity for All Investors Act (H.R. 3339) passed the House through a voice vote with suspension of rules. It’s already been sent to the Senate for consideration, been read twice and referred to the Committee on Banking, Housing, and Urban Affairs. This bill will pass and become law.

On paper, this bill sounds like a win for everyday Americans, especially when framed by its Democratic supporters.

“Our bill will unlock capital for entrepreneurs and small business owners who’ve been left out for far too long,” said Rep. McBride (D-Delaware), who co-sponsored the bill. “Current law allows only millionaires to invest in private markets—shutting out countless Americans especially women, veterans, and people of color, based on wealth, not knowledge.”

Sounds great, right? Fair? Putting we women, veterans, and people of color on a level playing field with billionaires and Wall Street? What could go wrong?

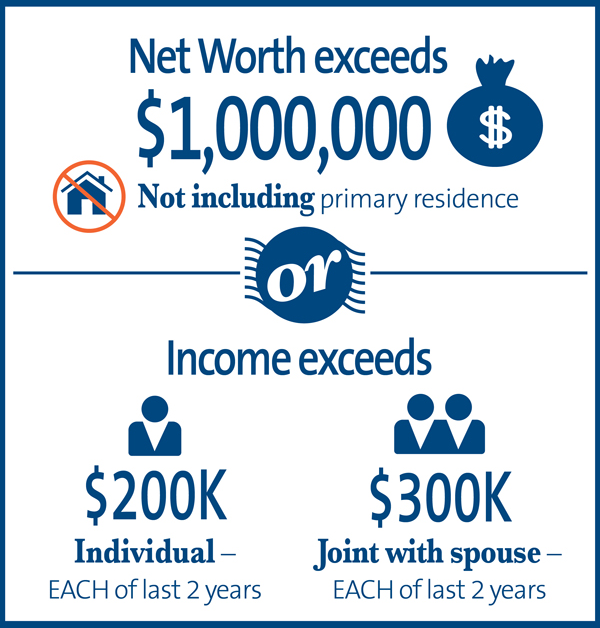

This bill allows individuals to qualify as “accredited investors” based on their financial knowledge, not their income or net worth. But it fails to mention those waiting behind the curtain: private equity firms. Those who feed off of turning other people’s money into their own profits, while leaving nothing but destruction in their wake.

Supporters claim this will “remove structural barriers” and create more diverse pools of investors, providing underserved entrepreneurs with badly needed funding. In McBride’s own state, she says the Delaware Black Chamber of Commerce believes the legislation would “help close the capital gap for diverse business owners.”

On the surface, this is dressed up as a way to democratize access to investment opportunities—particularly in high-risk industries like private equity. But come on, now. We know better. And if you don’t, you should.

This legislation is nothing more than a trap for the financially vulnerable. Think housing bubble, payday loans, our student loan crisis, MLM hooks. When we ‘democratize’ opportunity without any real safeguards, it always—always!—falls back on the very people it claims to ‘empower.’

Here’s how this bill works: instead of requiring investors to have a certain income or net worth (which was at least a basic safeguard), anyone with the right “knowledge” can now invest in high-risk, high-stakes, and often shady private equity deals.

And how does one gain this “knowledge?” By taking a test administered by the SEC. The Trump administration’s SEC.

This door is wide open for people with little financial security to take on massive risks they don’t fully understand, hoping to strike it rich—but most will get burned. Remember balloon mortgages?

It’s a dangerous game our democratic Congress and Senate are playing with vulnerable people. It’s almost like the promise of the American Dream, but on steroids. It’s sold as opportunity, but it’s built to strip protections and siphon off what little wealth the working-class has.

Supporters like McBride present the bill as a way to let more people “turn vision into jobs and economic growth.” But nothing in this bill forces that new capital toward Main Street instead of Wall Street.

This is nothing more than deregulation. And history tells us how that ends: from the junk bond boom in the ‘80s, to the rollout of Regulation Crowdfunding in 2016 (about 99% of offerings have yielded no returns to investors), to the largely unregulated explosion of cryptocurrency markets, to the wave of day traders losing their life savings on commission-free apps. Every single time, it’s overwhelmingly benefitted institutional players and wiped out the little guys. And with this bill, private equity firms are poised to rinse and repeat.

Just look at the Trump crypto coin. About 712,777 wallets—primarily belonging to small-scale holders—have collectively lost about $4.3 billion (yes, with a B). Meanwhile, just 45 wallets captured approximately $1.2 billion in gains.

Why does any sane person believe that this “opportunity” will be any different?

Firms will package high-risk investments, sell them to newly “qualified” investors, and promise big returns.

The reality?

The risk isn’t shared equally. The firms raising money still get paid through management fees, carried interest, and other compensation—whether the investments succeed or fail. The new “knowledge-based” accredited investors, especially those without real market experience, are the ones who take the hit when those bets go bad. And they will take the hit.

Multi-billionaires can afford to lose a billion dollars. The average Joe? Not so much.

And the worst part?

These investors will have no safety net, no protections, and no fallback when it all collapses. And it will. Some people will lose everything through this. People who cannot afford to lose everything.

Private equity thrives on this kind of access. Why do you think they aren’t against this bill? And why do you think it was passed without a recorded vote?

This bill gives private equity a bigger pool of targets, funneling money into predatory deals that exploit local businesses and inflate corporate profits—while the “investors” (those who really cannot afford it) are left holding the bag. We have another article coming soon on how private equity is buying up mom and pop HVAC, plumbing, and electrical businesses.

We’ve seen it all before. Now we’re seeing it with everyday people’s retirement savings and the financial future of thousands of Americans. This is their American Dream, not ours. The one that strips away any financial protections and puts the last of the working-class wealth at risk.

Let me be clear: I am not against the working and middle class having a fighting chance at building wealth. Nor am I against small business owners having more opportunities for equity. Like the majority of people in this country, I fall in those categories, and so does my family. I’m against opportunity without proper regulation to protect the working and middle class and small business from the very vultures that are currently eating us alive.

If history has taught us anything it is that if they are welcoming such a financial “opportunity” with open arms, it’s because they are the ones who will benefit. Not us. Especially, when we are in the end stages of capitalism.

This bill is just the latest in a long list of corporate-friendly laws where those who don’t need help get more of the pie, while the rest of us fight over the crumbs.

It’s just another ploy to take from the struggling, vulnerable, and desperate and give to the already obscenely rich. The lack of regulation is all the proof anyone should need. Encouraging people to invest in ‘opportunities’ they don’t understand is a recipe for unmitigated disaster.

Rep. McBride calls it “bipartisan, common-sense policy” that “creates opportunity, unlocks innovation, and expands prosperity.” In fact, every legislator I heard speak repeated the same rhetoric. And they all know exactly what they are doing. They also know that without strong safeguards (REGULATION) “opportunity” will mean the opportunity for Wall Street to raid the last unguarded vault of working-class savings.

This isn’t freedom. It’s financial exploitation disguised as inclusion and equal opportunity.

Coming next to a neighborhood near you: debtor prisons. So you can be their unpaid labor—expanding on the 13th Amendment.

Parody? Sure. But it’s the trajectory we are on.

Footnote: This vote was passed in the House by a voice vote under suspension of the rules. This means that there are no recorded “yeas” or “nays”—just a collective, unrecorded affirmation. Here is the video. The vote is around the 5:30 mark, but the commentary starts before that. I can’t hear the responses to the vote, but since all the politicians are speaking in favor of it, it seems that it’s 100% yeas.

This sets the stage for plausible deniability. We need a better system.