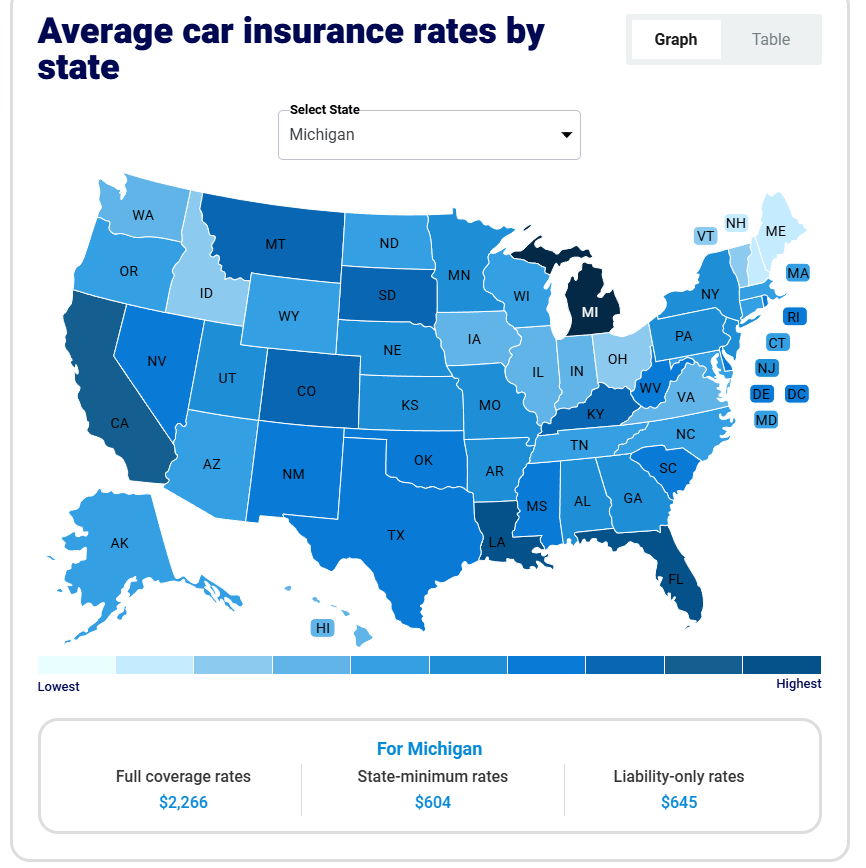

The Unfulfilled Promise of Michigan’s Auto Insurance Reform

Everyone in Michigan feels the weight of high auto insurance costs—but the burden falls heaviest on retirees, working-class families, low-income workers, and new drivers. They’re being forced to pay exorbitant monthly rates just to survive in a state with no viable public transit and no real way out.

This crisis hit home when my own family began searching for affordable coverage—and came up empty. That experience led me to dig deeper into an industry that has quietly fleeced Michiganders for decades in a state with some of the highest auto insurance rates in the country. These are my findings.

The Genesis of Reform

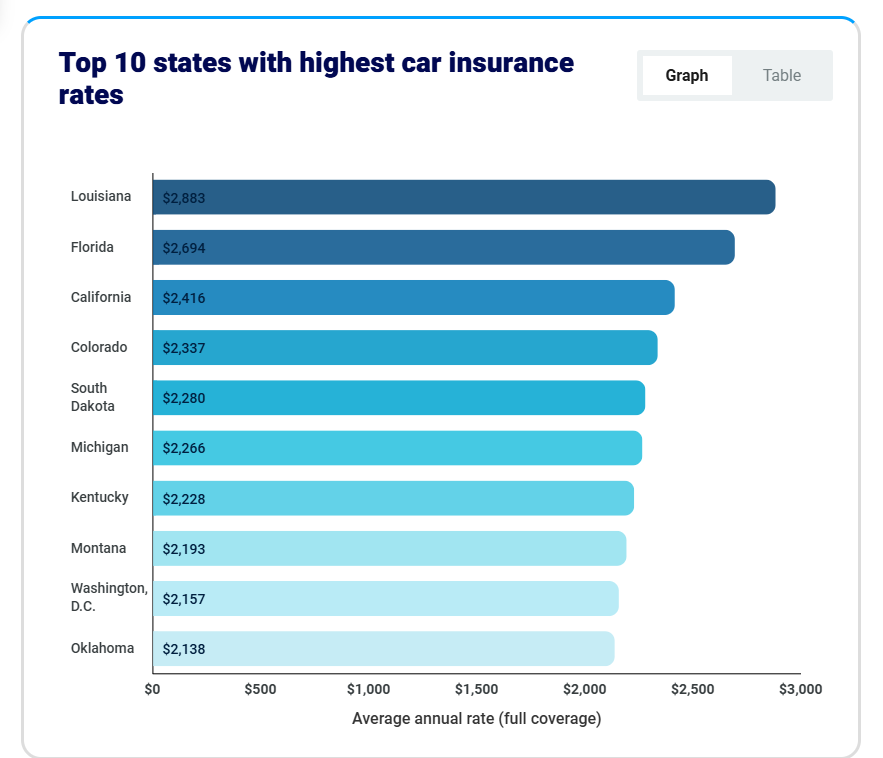

In 2019, Michigan lawmakers heralded a new era for drivers across the state with the passage of auto insurance reform aimed at reducing the notoriously high premiums that had burdened residents for decades. The reform was designed to offer choices, lower costs, and eliminate discriminatory practices in rate-setting. But a handful of years later, many Michiganders—especially seniors on Medicare, working families, low-income workers, and new drivers (nearly 50% of the population)—find themselves grappling with the same unaffordable rates, or worse. The reform promised change. What it delivered was confusion, loopholes, and more hardship.

Persistent Financial Strain on Vulnerable Populations

Despite structural changes, the relief promised by the 2019 reform has not reached the people who need it most.

Retirees on Medicare were supposed to be the big winners under the new law. The legislation allowed seniors with Medicare Parts A and B to opt out of costly PIP (Personal Injury Protection) medical coverage. But in practice, many seniors enrolled in Medicare Advantage plans found out that their coverage doesn’t include auto accident injuries (my mother being one). With no guarantee of protection, insurers deny the opt-out. Seniors are then forced to carry expensive PIP policies they don’t need and can’t afford. For someone on a fixed income of $1,800 a month, a $400 insurance bill isn’t just unaffordable—it’s devastating.

Michigan has roughly 2.26 million Medicare enrollees, representing nearly 22% of the state’s population (MHA). In a state with virtually no dependable public transportation system, a large percentage of these seniors still rely on their cars to access medical care, grocery stores, or family support. Yet they’re being hit with sky-high premiums for coverage they already pay for through federal health programs—just because their insurers refuse to acknowledge it.

Low-income families and Medicaid recipients face a different kind of trap. Michigan has 2.7 million Medicaid enrollees, about 27% of the population, and many of them work full-time. A University of Michigan study found that 44% of Medicaid expansion enrollees are employed, and more than half of them work full-time (IHPI). Yet even those working 40 hours a week are priced out of basic transportation. While Medicaid recipients can opt for a lower $50,000 PIP cap, this is often insufficient in severe accidents—and overall rates still remain out of reach for many.

New and young drivers are also being priced out of the system. First-time drivers are often quoted $300 to $700 a month—an impossible amount for most teenagers or young adults who need transportation to attend school or work (at 19, my son was quoted between $424-$725). In effect, Michigan’s current system penalizes you for being young, poor, or retired.

The Public Transportation Conundrum

The lack of affordable auto insurance might be manageable if Michigan had a reliable, timely public transportation system—but it doesn’t. Outside of a few select corridors in Detroit and Ann Arbor, public transit is not a viable option for most Michiganders. Bus service is infrequent or entirely absent in many areas, and regional systems are fragmented and unreliable. There’s also no high-speed rail connecting Michigan’s major cities, leaving residents with few practical alternatives to driving.

This means car ownership is not optional—it’s a requirement for life in Michigan. When driving becomes mandatory and insurance becomes unaffordable, what choice do people really have?

For the nearly 50% of Michigan residents who are either seniors on Medicare, working-class and low-income recipients, or young drivers trying to establish financial independence, this is not just inconvenient—it’s oppressive.

Discriminatory Practices and Rate Disparities Persist

The 2019 reform also promised to eliminate the use of non-driving factors like ZIP codes, credit scores, and education levels when setting rates. But insurers quickly found workarounds.

According to research from the University of Michigan’s Poverty Solutions initiative, residents of predominantly Black and working-class communities still pay significantly more for car insurance—even when controlling for driving history. In Detroit, average premiums still top $5,000 a year (Poverty Solutions).

State Senator Jeff Irwin (D-Ann Arbor) acknowledged these ongoing problems in a 2021 interview:

“Insurance companies already knew that they were going to be able to get around it.”

The result? A discriminatory pricing model that punishes people for where they live, how much money they make, and what kind of coverage they don’t need.

The System Is So Broken,

People Are Forced to Break the Law

When insurance becomes unaffordable, people stop buying it. Not because they want to break the law—but because they have no other choice. Michigan continues to lead the nation in the number of uninsured drivers.

As many as 1 in 4 vehicles on the road in Michigan may be uninsured. (Michigan Auto Law).

This is the inevitable result of bad policy: people are forced to choose between buying groceries, paying rent, or purchasing legally required auto insurance. In most cases, survival wins—and legality loses.

And that hurts everyone:

- Uninsured drivers lead to higher rates for everyone else.

- Accident victims hit by uninsured drivers face lawsuits, limited payouts, or financial ruin.

- The entire system becomes unstable—pushed to its limits by people who were never given a fair chance to participate in the first place.

I saw the consequences of this broken system firsthand. In 2023, my son was in a car accident while at work. He was a passenger in a company truck that was hit by another driver—who was at fault. He received care at a local clinic, including X-rays for his knees after they slammed against the console, and was placed in a knee brace for a week. The bill, totaling over $1,500, was submitted to his employer’s insurance provider—Progressive—under the assumption it would be covered as a work-related injury. Months later, it came back denied. Progressive claimed that because he wasn’t the one driving, he wasn’t covered. We are still fighting this, both with his employer (former) and with Progressive, and we are now preparing to go after the at-fault driver’s insurance company as well.

This is how broken the system is—even when someone is clearly injured, not at fault, and acting within the scope of their job, they can still be left holding the bag.

The Role of For-Profit Healthcare in Driving Up Costs

The auto insurance crisis in Michigan is further amplified by the underlying structure of our healthcare system. For decades, Michigan’s unique no-fault insurance laws (that’s not a compliment) required auto insurers to cover all medical costs for accident victims, often with no cap and no negotiation. As a result, healthcare providers routinely charged auto insurers significantly higher rates than they charged Medicare or private health insurance companies (CRCMich).

In response, the 2019 reform introduced a fee schedule in 2021 that capped what providers could bill auto insurers, linking it to Medicare rates (Milliman). But this fix did little to address the root problem—the sky-high cost of medical care driven by our for-profit healthcare system. Hospitals, rehab centers, and private providers all price services to maximize profit, not affordability.

So even when PIP costs are capped, the base cost of medical care remains inflated. And because insurers are on the hook for these inflated costs, they simply pass the burden onto drivers—raising premiums across the board.

Until we tackle the greed baked into our medical pricing system, Michigan’s insurance crisis will remain unsolvable.

Political Complicity and Industry Influence

So how did we get here?

The 2019 reform was signed into law by Democratic Governor Gretchen Whitmer. It passed with bipartisan support, but it was written and pushed forward by Republican legislators and backed heavily by the insurance industry.

Democrats touted the bill as progress. Governor Whitmer highlighted the bipartisan effort, stating:

“In 2019, Republicans and Democrats in the Legislature and I came together to deliver historic, bipartisan auto insurance reform that lowered costs for drivers…”

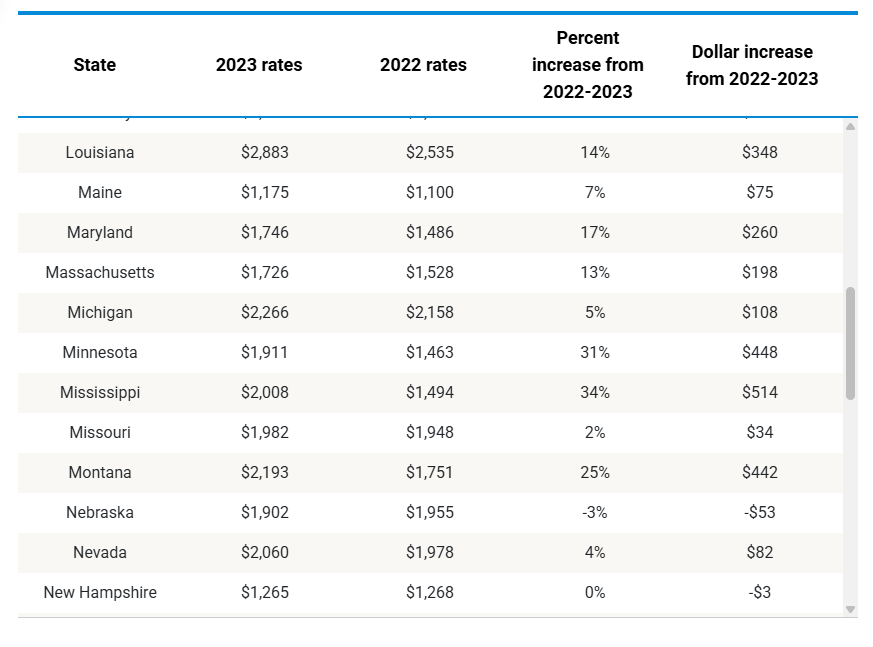

But in the years since its passage, growing concern has emerged over how the reform has played out—particularly as some insurers, instead of lowering premiums, actually raised rates. For example, Citizens Insurance—a Michigan-based provider—increased average premiums by $90 after the law took effect, according to data reported by the Consumer Federation of America (WXYZ). Douglas Heller, the group’s Director of Insurance, noted that this reflects a broader pattern of insurers shifting costs rather than delivering savings.

While there are no public statements from Democratic lawmakers explicitly saying they were misled, many have acknowledged that the reform has failed to bring the relief it promised. Others have shown reluctance to revisit the legislation—potentially due to donor pressure or political risk. We all know that this is far more important to the average legislator than legislation that actually works for We the People.

Republicans, for their part, celebrated the reform as a win for consumer choice. But Senate Majority Leader Mike Shirkey made it clear the priority was protecting insurers, stating:

“The goal is simply to provide consumers with options so they can choose how much they want to spend.”

(Quote via Bridge Michigan)

What he didn’t mention:

most people have no meaningful choice at all—because the coverage they already pay for (Medicare, Medicaid, or private health insurance) doesn’t qualify them for an opt-out.

Meanwhile, insurance industry donations at the state level flooded key lawmakers’ campaign accounts:

- Tom Leonard, then-House Speaker (R-DeWitt), received $104,275 in campaign contributions from the insurance industry from 2011 through 2017.

- Lana Theis, House Insurance Committee Chair (R-Brighton) and sponsor of House Bill 5013 (A bill to amend 1956 PA 218, entitled “The insurance code of 1956), received $27,900 in campaign contributions from the insurance industry from 2013 through 2017. (Michigan Auto Law)

- Earlier efforts like Senate Bill 248 (SB 248) in 2015 saw similar trends: Senator Joe Hune received $108,075, and the bill’s only Democratic supporter, Senator Virgil Smith, took in $36,800. (Auto No-Fault Law)

At the national level, the insurance industry contributed $24.6 million during the 2023–2024 election cycle—$13.8 million to Republicans and $10.7 million to Democrats (OpenSecrets).

And while Governor Whitmer did not receive outsized direct donations from insurance companies in her re-election campaign, she did receive $58,000 from Blue Cross Blue Shield of Michigan and $10,000 from the Auto Club of Michigan.

But that’s not the full picture.

A nonprofit closely tied to her—Road to Michigan’s Future—quietly raised $12.9 million in 2022 from undisclosed donors. Because it’s a 501(c)(4), the public has no right to know who gave the money or what they expected in return (Detroit News). This is how modern political influence works—not just through campaign checks, but through anonymous millions funneled into nonprofits that operate entirely in the shadows.

When both parties are funded by the same industry they’re supposed to regulate—whether out in the open or behind closed doors—it’s no surprise the result is a law that benefits corporations over constituents.

What Can You Do?

This fight isn’t just about bad policy—it’s about a system rigged to serve profit over people. But you’re not powerless. Here’s where you start:

- Demand legislative accountability. Call your state reps. Email the governor’s office. Show up at town halls. Force them to answer for this mess—and to fix it. Download email and call script, along with list of who to contact below.

- Push for real transparency. No more secret donors. No more dark money nonprofits. We need legislation that requires full disclosure of political spending—regardless of the loophole.

- Organize locally. Join or form coalitions with others affected by high insurance rates. Whether you’re a retiree, a working parent, a young driver, or someone living with a disability—your story matters. Together, we become harder to ignore.

- Support ballot initiatives and reform candidates. If the legislature won’t act, the people can. Michigan voters have used ballot proposals to change the law before. It can happen again.

- Tell your story. Share how these policies are hurting your family, your finances, your future. Post it. Publish it. Talk about it. This isn’t just policy—it’s personal.

Because the truth is this: we were never meant to win under a system built like this. But we can fight. And when we fight together—loud, relentless, and unapologetic—we can break it open.

Download email and call script below.